Student Finance Explained: Loans, Repayment & Eligibility

By Michael Thompson · Former IB Diploma Programme coordinator; 10 years at Bromsgrove School · Published 5 July 2026

Student finance is the government-backed system that covers tuition fees and living costs for eligible UK students entering higher education - you borrow the money, the university is paid directly for fees, and you repay only once your earnings pass a threshold. For most English undergraduates starting in 2026, that means a Tuition Fee Loan of up to £9,790 per year plus a means-tested Maintenance Loan to cover rent and living costs. The two parts work differently: the fee loan is fixed by where you study, while the maintenance loan depends on your household income and where you live. This guide covers how each part works, who qualifies, what repayment looks like, and what to do if you are an international or overseas student wondering whether the system applies to you.

Key Takeaways

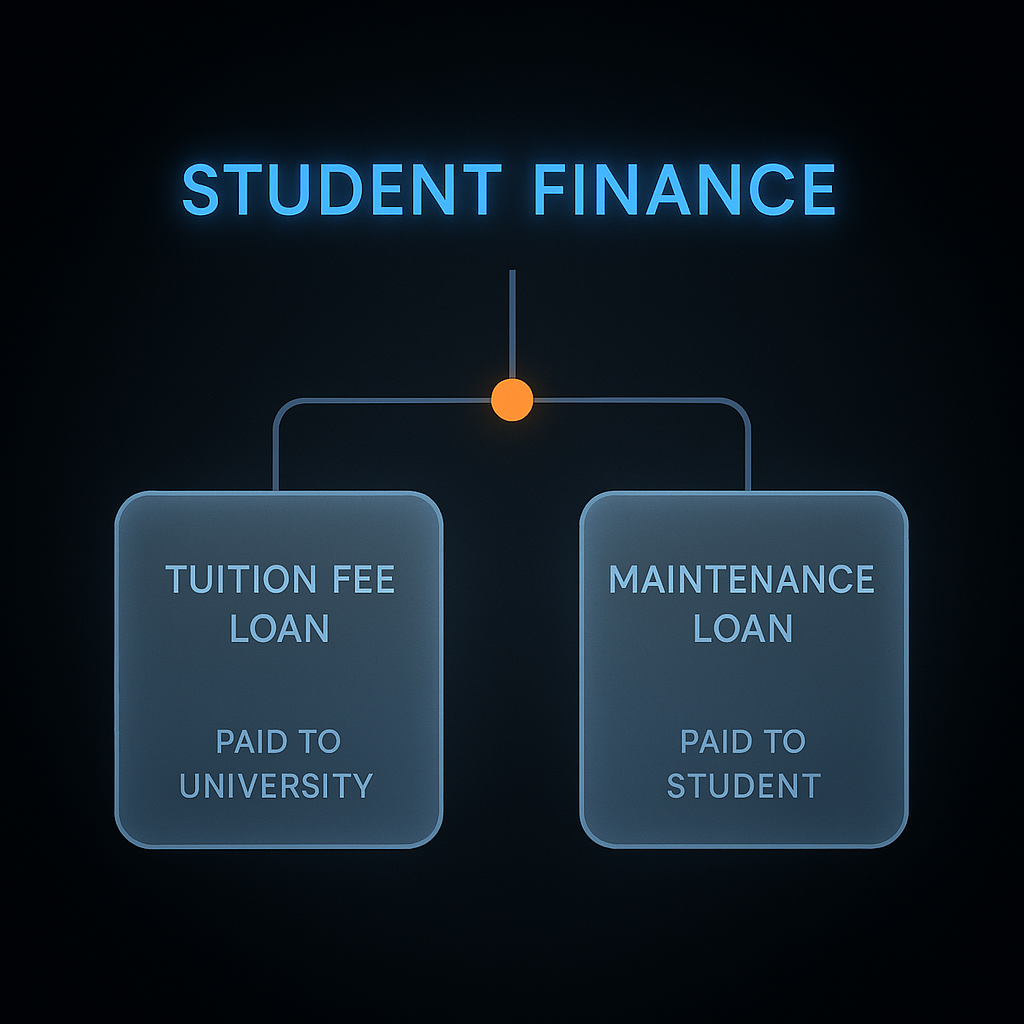

- Two separate loans: Student finance splits into a Tuition Fee Loan paid directly to your university and a Maintenance Loan paid into your bank account each term.

- Maintenance loan is means-tested: The amount you receive depends on household income, meaning students from higher-income families receive less - and parents are not legally required to make up the shortfall.

- Repayment starts only above the earnings threshold: For Plan 5 borrowers (English starters from 2023 onwards), repayments begin the April after leaving your course, but only if your income exceeds the threshold set for that year.

- Fee status determines whether you qualify at all: Home, international, and overseas students face very different fee levels; the loan system applies to home-fee students only, based on residency rules - not just nationality.

- Each UK nation runs its own system: England, Scotland, Wales, and Northern Ireland have separate student finance bodies, different amounts, and different deadlines - the figures in this guide apply to English-domiciled students.

- Application deadlines matter: The Student Finance England deadline for 2026/27 full-time applications is 15 May 2026, but late applications are still accepted.

In This Article

- What Student Finance Is and How the Two Parts Work

- Tuition Fee Loan: Amounts, Caps, and What They Cover

- Maintenance Loan Amounts and How Household Income Affects Them

- Student Loan Repayment: Plan, Threshold, and Write-Off

- Fee Status: Home, International, and Who the Loan System Covers

- England, Scotland, Wales, and Northern Ireland: Four Separate Systems

- Will Student Finance Fund a Second Degree, a Masters, or a Repeat Year?

- How to Apply: Deadlines, What You Need, and Tracking Your Application

- What to Do Next

1. What Student Finance Is and How the Two Parts Work

Student finance is the government-backed system that funds UK students through higher education. It has two separate loans: a Tuition Fee Loan, paid directly to your university, and a Maintenance Loan, paid to you in three instalments across the academic year. Neither requires any upfront payment, and repayment only starts once you leave your course and earn above a set threshold.

The Tuition Fee Loan

The Tuition Fee Loan covers what your university charges for teaching. The money never passes through your hands - Student Finance England pays the institution directly. For 2026/27, the maximum is:

- £9,790 per year for a standard full-time degree

- £11,750 per year for an accelerated degree

- £7,335 per year for part-time study

Because the loan matches the fee cap exactly for most courses, the majority of full-time students simply apply for the full amount and never have to think about the gap.

The Maintenance Loan

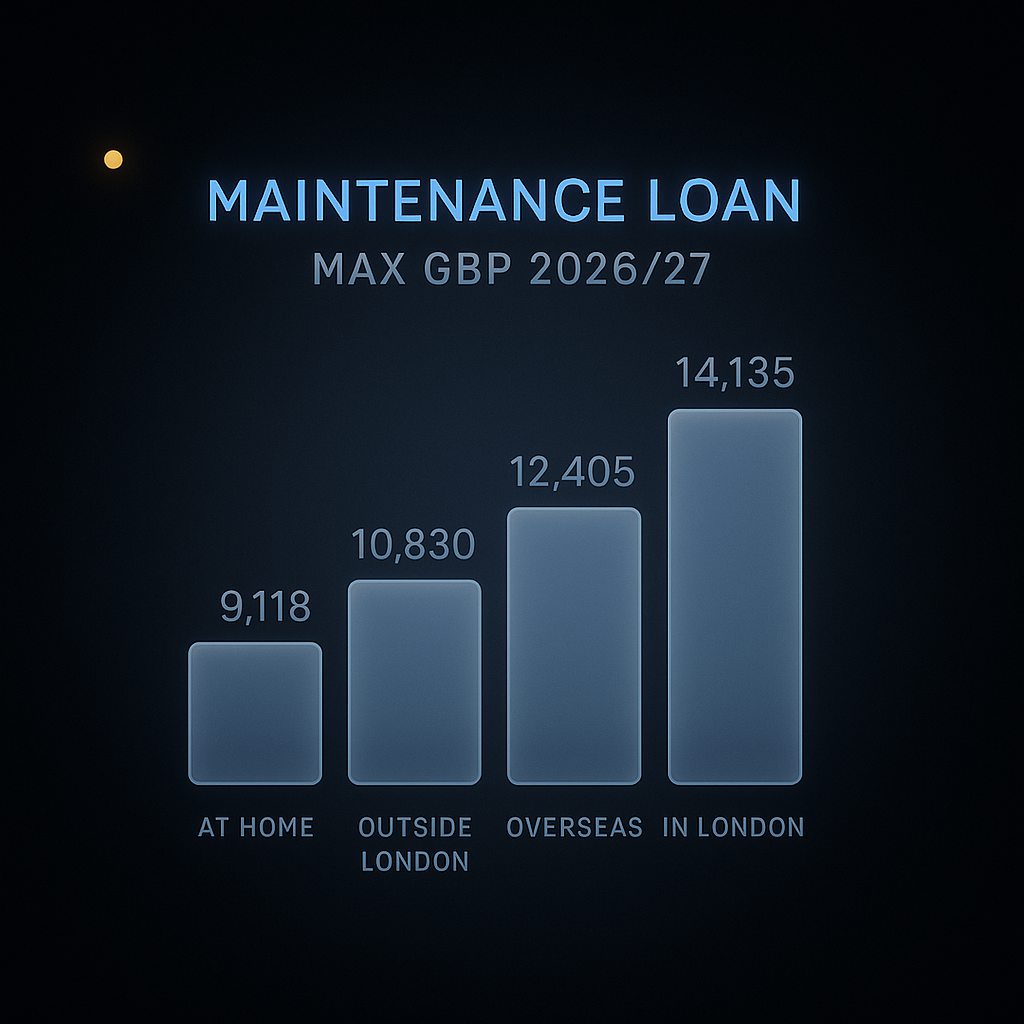

The Maintenance Loan covers living costs - rent, food, travel, books. It is paid directly to you, split across three term-time instalments. The amount is set annually and varies depending on where you study, whether you live at home, and your household income. For 2026/27, the maximum for a student studying outside London and not living with parents is £10,830.

One detail worth knowing: the Maintenance Loan is means-tested, but the Tuition Fee Loan is not. You get the full Tuition Fee Loan regardless of what your parents earn. The Maintenance Loan shrinks as household income rises - so two students on the same course at the same university can receive very different amounts of cash in hand each term.

Neither loan triggers repayment until after you leave or finish your course and your income exceeds the repayment threshold. The two loans are separate debts with separate mechanics, which matters when it comes to interest and write-off rules covered later in this guide.

2. Tuition Fee Loan: Amounts, Caps, and What They Cover

The Tuition Fee Loan covers your university or college fees directly. You never handle this money: it goes straight to the institution on your behalf, which means you cannot accidentally spend it and there is no interest-free window to game.

For 2026/27, the fee caps are set as follows, per UCAS:

| Course type | Maximum Tuition Fee Loan |

|---|---|

| Full-time undergraduate | £9,790 per year |

| Part-time undergraduate | £7,335 per year |

| Accelerated degree | £11,750 per year |

| Foundation year (classroom-based) | £5,760 per year |

| Foundation year (partly practical) | £9,790 per year |

These figures are subject to Parliamentary regulations being laid in early 2026, so treat them as expected rather than confirmed until that happens.

The loan covers fees up to the cap. If your institution charges above the cap, the difference comes out of your own pocket. This is most likely to affect part-time students at private providers, where fees can exceed the £7,335 ceiling.

One non-obvious detail: foundation year fee caps split by subject type, not by institution. A foundation year in business or humanities sits under the lower £5,760 cap, while one in science or engineering qualifies for the higher rate. Check which category your specific course falls into before assuming the full loan will cover your fees.

Amounts are reviewed each academic year and can change, so always confirm the current cap on GOV.UK before you apply.

3. Maintenance Loan Amounts and How Household Income Affects Them

The maintenance loan max amount you can receive depends on where you live and study, and for most students, on your household income. The higher your household income, the less you receive. For 2026/27, the full-time maximums are:

| Living situation | Maximum loan (2026/27) |

|---|---|

| Living with parents | £9,118 |

| Outside [London, not with parents](/guides/best-student-cities-uk) | £10,830 |

| London, not with parents | £14,135 |

| Studying/living abroad as part of a UK course | £12,403 |

Final-year students receive a reduced amount, because their year is shorter. The 2026/27 final-year maximums are £8,579 (with parents), £10,242 (outside London), £13,096 (London), and £11,103 (abroad).

The parental-contribution gap is the most under-discussed problem in student finance. As household income rises, the loan tapers down, with the assumption that parents will make up the difference. There is no legal mechanism to enforce this. If a parent chooses not to contribute, or cannot, the student simply has less money. Nothing in the system corrects for that.

Two groups are protected from this dynamic. Care leavers receive the maximum maintenance loan regardless of household income. Estranged students, defined as those who have had no contact with either parent for 12 months or more, do not need to submit parental income information at all, which means their loan is assessed independently.

Amounts are set each academic year, so the figures above apply to courses starting in 2026/27 and may change for subsequent years.

4. Student Loan Repayment: Plan, Threshold, and Write-Off

English undergraduates who started from 2023 onwards are on Plan 5. The mechanics are straightforward, but one detail catches people out: repayment is income-contingent, meaning you pay nothing until your earnings cross the threshold, regardless of how large the loan has grown.

When repayment starts: repayment begins the April after you leave or finish your course, but only once your income exceeds the current threshold. Per UCAS, this applies to both tuition fee and maintenance borrowing combined.

The rate: you repay 9% of everything you earn above the threshold. Nothing below it is touched.

The threshold itself changes. It is reviewed annually, so any figure printed here would be out of date within months. Check the current number directly on GOV.UK before making any financial plans.

Interest accrues throughout your studies and repayment period. For Plan 5, the rate is linked to RPI or a capped measure, and it also changes. Again, check GOV.UK for the current figure.

The write-off quirk: Plan 5 has a 40-year write-off period, longer than the 30 years that applied to Plan 2 borrowers. For graduates on modest-to-average salaries, this means more years of repayment before any balance is cleared, and the total repaid over a lifetime can exceed the original loan. High earners who repay quickly may pay less overall. The write-off date is fixed from when repayment was due to start, not from when you actually began paying.

| Plan | Repayment starts | Rate above threshold | Write-off period |

|---|---|---|---|

| Plan 5 (England, 2023 entry onwards) | April after leaving or finishing | 9% | 40 years |

The threshold and interest rate are reviewed annually. Always verify current figures on GOV.UK.

5. Fee Status: Home, International, and Who the Loan System Covers

The student finance loan system is built around fee status, not nationality. If you are classed as a home student, you pay the regulated tuition fee and can apply for SFE loans. If you are classed as international or overseas, you pay a higher unregulated fee set by the university, and SFE loans are not available to you at all.

Residency is what determines fee status, not your passport. Per the GOV.UK student finance guide, to qualify for full support, you must have lived in the UK, Channel Islands, or Isle of Man for the three years immediately before your course start date, and England must be your home address for reasons other than study.

The following groups are eligible for full support:

- UK nationals who meet the residency requirement

- Irish citizens

- Those with settled status under the EU Settlement Scheme

- Those holding refugee status, humanitarian protection, or stateless status

- Those with leave under the ARAP, ACRS, ARR, or Ukraine schemes (Family, Homes for Ukraine, or Ukraine Permission Extension)

The non-obvious gotcha: the three-year residency clock applies to where you actually lived, not where you hold citizenship. A British national who has spent the last three years abroad, including internationally mobile students who studied an IB Diploma Programme at a school outside the UK, may not automatically qualify. They would need to demonstrate that their UK address is a genuine home, not just a study base. If you are in that situation, check your status with SFE before assuming you are covered.

International and overseas students who do not meet these conditions must fund study through other routes: university scholarships, government-sponsored loans from their home country, or private finance.

6. England, Scotland, Wales, and Northern Ireland: Four Separate Systems

The figures throughout this article apply to **English-domiciled students applying through Student Finance England (SFE)**. Each UK nation runs its own student finance body with its own amounts, grants, and rules, so checking the right one matters.

The counter-intuitive part: **your domicile, not your study location, determines which system applies.** An English student studying at the University of Edinburgh applies to SFE, not SAAS. A Welsh student at a London university applies to Student Finance Wales. Getting this wrong means applying to the wrong body entirely.

| Nation | Body | Notable difference | 2026 deadline |

|---|---|---|---|

| England | Student Finance England | Standard loans; no non-repayable grant for most students | 15 May 2026 |

| Wales | Student Finance Wales | Tuition Fee Loan plus the Welsh Government Learning Grant (non-repayable) | 29 May 2026 |

| Northern Ireland | Student Finance Northern Ireland | Separate body, different loan amounts | 30 April 2026 |

| Scotland | SAAS (Student Awards Agency Scotland) | Different structure; tuition is free for eligible Scottish-domiciled students | Check SAAS directly |

The Welsh Government Learning Grant is worth flagging: unlike a loan, it does not require repayment, which meaningfully reduces the total debt Welsh students accumulate compared to their English peers.

Check the correct body for your home nation before applying.

7. Will Student Finance Fund a Second Degree, a Masters, or a Repeat Year?

Student finance does not automatically follow you into a second qualification. The rules differ significantly depending on whether you are returning to undergraduate study, repeating a year, or moving to postgraduate level.

Second degree

The most common misconception: if you already hold a degree (or an equivalent Level 6 qualification), you are generally not eligible for standard undergraduate tuition fee and maintenance loans for a second undergraduate degree. There are narrow exceptions, for example some healthcare courses, but the default position is no funding. Check your specific situation on GOV.UK before assuming you qualify.

Repeat year

Student finance can cover a repeat year, but only in limited circumstances. The rules hinge on whether the repeat was caused by compelling personal reasons rather than straightforward academic failure. The specifics are detailed and change, so use GOV.UK as your primary source.

Masters and doctoral loans

These are entirely separate products from undergraduate student finance, administered through Student Finance England. Neither is means-tested, so household income does not affect the amount.

| Loan | Maximum (courses from 1 August 2026) | Means-tested? |

|---|---|---|

| Postgraduate Master's Loan | £13,206 | No |

| Postgraduate Doctoral Loan | £31,122 | No |

One non-obvious point: doctoral loan applicants who apply after their first year of study may not receive the maximum amount, so applying early matters in a way it does not for undergraduate loans.

Repayment for the Master's Loan begins from April after you leave or finish your course, provided your income exceeds the repayment threshold. Applications for 2026/27 open the week commencing Monday 20 July.

8. How to Apply: Deadlines, What You Need, and Tracking Your Application

The Student Finance England deadline for 2026/27 full-time undergraduates is 15 May 2026. Applications cover courses starting between 31 August and 31 December 2026, and SLC states processing takes six to eight weeks, so applying early reduces the risk of delays at enrolment.

The counter-intuitive detail most students miss: you do not need a confirmed university place before applying. Course details can be updated after you receive offers, so there is no reason to wait for Firm Choice before submitting.

What you need before you start:

- National Insurance number, obtainable via the HMRC app if you do not already have it to hand

- Passport

- Bank account details for payment

Applications are made at gov.uk/student-finance, and progress is tracked through your online account. SLC advises students not to contact them directly just to check status - the account view covers that.

Missing the 15 May deadline does not close the door - late applications are accepted, though payment at the start of term becomes less certain.

One significant boundary to note: if your course starts on or after 1 January 2027, standard student finance does not apply. You will need to apply through the Lifelong Learning Entitlement instead, with LLE applications expected to open from September 2026.

9. What to Do Next

If your course starts between August and December 2026, the most important thing you can do this week is apply. Student Finance England opened applications on 23 March 2026, and the deadline is 15 May 2026. Processing takes up to six to eight weeks, so late applications risk your money not arriving for day one of term.

One non-obvious point: you do not need a confirmed university place to apply. Submit now with your expected course details and update them later. Waiting for a firm offer is a common reason students miss the deadline unnecessarily.

Once your application is in, start planning your university choices. Visit our UCAS hub covering the full application process, deadlines, and offer types to make sure your course and fee status align with what your loan will actually cover.

Apply at gov.uk/student-finance before 15 May 2026. Track progress through your online account rather than contacting SLC directly.

FAQ

How much student finance can I get?

For 2026/27, English full-time undergraduates can borrow up to £9,790 in a Tuition Fee Loan plus a Maintenance Loan of up to £14,135 (London rate), though the maintenance amount is means-tested against household income and most students receive less than the maximum.

What student finance plan am I on?

English undergraduates who start their course from 2023 onwards are on Plan 5; the plan determines your repayment threshold, the write-off period, and how interest accrues - check your Student Finance England account or gov.uk to confirm your plan.

How is student finance paid?

The Tuition Fee Loan is paid directly to your university at the start of each term; the Maintenance Loan is paid into your bank account in three instalments, one at the beginning of each term, after your attendance is confirmed.

Will student finance fund a second degree?

In most cases, no - if you already hold an equivalent or higher qualification, you are not eligible for standard undergraduate student finance for a second degree, though limited exceptions exist for certain healthcare and teaching courses.

Will student finance fund a Masters?

Undergraduate student finance does not cover a Master's degree; instead, a separate Postgraduate Master's Loan of up to £13,206 (for courses starting on or after 1 August 2026) is available, and it is not means-tested.

How does student finance affect Universal Credit?

The Maintenance Loan counts as income for Universal Credit purposes, which can reduce the amount of Universal Credit you receive; the rules on how each element of student finance is treated are set by the DWP and are worth checking directly on gov.uk before applying.

References

- Student Finance - Student Loans And Tuition Fees - https://www.ucas.com/student-finance/tuition-fees-and-tuition-fee-loans

- Maintenance loans, maintenance & support grants - Student living costs - https://www.ucas.com/student-finance-england/living-costs-full-time-students

- Student finance for undergraduates: Part-time students - GOV.UK - https://www.gov.uk/student-finance/parttime-students

- Student finance: how you're assessed and paid 2026 to 2027 - GOV.UK - https://www.gov.uk/government/publications/student-finance-how-youre-assessed-and-paid/student-finance-how-youre-assessed-and-paid-2026-to-2027

- Full-time undergraduate student finance applications now open for 2026 to 2027! - GOV.UK - https://www.gov.uk/government/news/full-time-undergraduate-student-finance-applications-now-open-for-2026-to-2027

- Starting uni or college in 2026 or 2027 - Student Finance England - https://studentfinance.campaign.gov.uk

- Postgraduate Master's Loan - help with living & course costs - https://www.ucas.com/student-finance-england/postgraduate-masters-loan